Alright, let’s get to it. If you Google search and chance upon this article, you probably know by now that there have been some changes to your integrated shield plans after 1st of April 2021. So how exactly does this change affect you especially if you have been a policy holder of your respective insurer integrated shield plan since before March 2018?

This article is for general information only it is not an advise nor does it take into account the specific investment objectives, financial situation or needs of any particular person. Read our General Disclaimer

Before we look into the integrated shield changes, it is important to note that there are also some major changes made to Medishield Life plan also, here are the changes made to Medishield life in point form since 1st March 2021

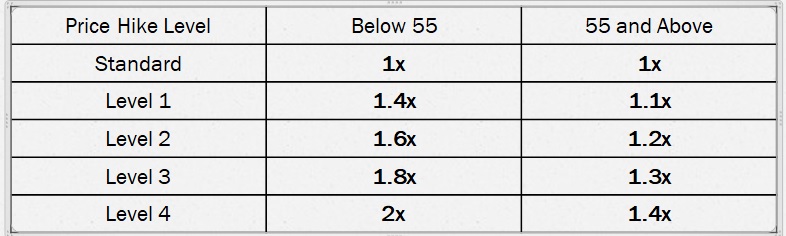

As announced in 2018, there will no longer be riders that will cover 100% of hospitalisation expenses, these riders are now defunct. Instead, all major insurers now provides a rider that will cover a maximum of 95% of the hospitalisation expenses. There will also be a cap on the 5% co insurance at $3,000 if the life assured seeks treatment within the provider’s list of panelled doctors in a private hospital or any doctors at a restructured hospital. The new rider also subject treatment done via a non-panelled private hospital doctor will have no cap and deductibles may be imposed even with the most comprehensive rider purchased.

We provide a breakdown of the individual Integrated Shield Plan provider changes in particularly if your plan is purchased before March 2018 and after and explain how you will be affected after 1st April 2021.

PS: We will only discuss on the most comprehensive rider for private hospital plans.

All Max Essential A riders owner will automatically be converted to AIA’s new claim base pricing rider Max VitalCare upon renewal after 1st April 2021. However, policyholder will still have the option to switch to AIA Max VitalHealth (95% rider) without medical underwriting before 30th September 2022

There will be no changes to your plan, however, you will have the option to switch to AIA Max Vital Care without medical underwriting before 30th September 2022

All Basic Care/General Care/Home Care Rider will automatically be converted to Enhanced Care Rider with 95% Co insurance, you will be subjected to a deductible of $1,500 if you seek treatment at a non-panelled doctor.

Your Enhanced Care Rider will remain, there will be price hike upon renewal after1st April 2021

Your MyHealthPlus Option C will be converted to MyHealthPlus Option C-II, C-II will imposed the 5% co insurance on your claim as well as a mandatory deductible of $500 if you apply for pre-authorisation before claim and a deductible of $1,000 if you did not apply for pre-authorisation or seek treatment with a non-panelled doctor

Your Option C-II rider will remain.

All private hospital riders regardless of version will be converted to the Great total care rider where claim based pricing will be enforced. A 5% co pay will also be automatically included in the new plan. There will be no limit to the co-payment of 5% should the policy holder seek treatment at a non-panelled specialist.

Your Total Care Rider will automatically be converted to a claim base pricing model, the 5% co-payment with cap @ $3,000 if you seek treatment at a panelled specialist, there will be no capped to the 5% co-payment should the insured seek treatment at non panelled specialist.

Your Plus Rider will automatically be converted to the Deluxe Care Rider on your next renewal after 1st April 2021, A 5% co insurance will be imposed on your claim. The 5% will have a cap of $3,000 for panelled doctor and no cap if you seek treatment via a non-panelled doctor. The Assist Rider will be converted to the Classic Care Rider, 10% co insurance will continue to be imposed, and there will also be a deductible of $2,000 if you seek treatment at a non-panelled doctor under the Classic Care Rider.

Your Deluxe Care and Classic Care Rider remains.

Your Prushield Premier with Pru Extra rider will continue to provide 100% even beyond 1st April 2021, this is the only insurer that continues with the 100% as charged coverage, the prushield extra is the pioneer of the claim base pricing structure starting all the way back since May 2017.

You will be covered under the Pru Extra (Co pay) version where 5% of the hospitalisation bill is payable by you. No cap to 5% if treatment is done via a non-panelled specialist, otherwise cap of $3,000/yr co pay applies.

Your raffles shield plan remains as it is, there was never a 100% covered rider to begin with. Raffles Shield Key rider provides 95% coverage feature with a 5% co insurance @ $3,000 cap. There will be no capped to the 5% if treatment is not pre authorised or treatment is done via a non-panelled specialist.

No changes to the initial plan bought before or after March 2018

Seek advise to get the most important coverage of your life

A Licensed Planner will contact you to provide you more information on the latest changes to your plan. Read our privacy policy

Comments are closed.

1 Comment