Compare Best Diabetes Insurance Singapore (2024) We Compare over 15 Life insurers to get you the best diabetes insurance plan in Singapore Learn about the different…

If you’re wondering if Medishield Life itself is sufficient for hospitalisation coverage and what is the best hospitalisation shield plan in Singapore, this article will help touch on and address the key feature of shield plans across different insurers

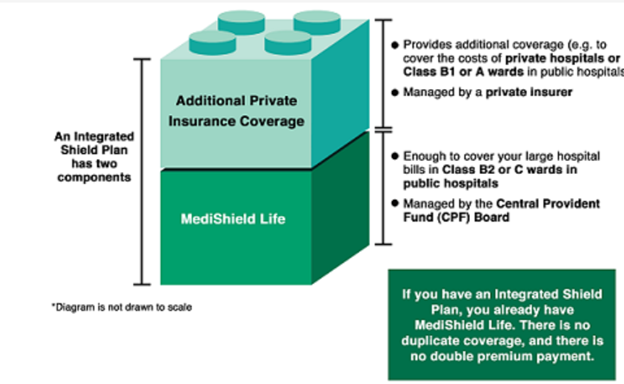

MediShield Life is a compulsory basic health insurance plan for Singaporean/PR, administered by the Central Provident Fund (CPF) Board, which helps to pay for large hospital bills and selected costly outpatient treatments, such as dialysis and chemotherapy for cancer. Its aim is to reduce the medisave/cash needed to pay for large hospitalization bill.

Medishield Life together with additional private insurance coverage makes up an Integrated Shield Plan (IP). It is optional and can be paid using medisave subjected to withdrawal limits.

– As charge coverage for public and private hospitals

– Pre/post hospitalisation claim

– Providing a higher per policy year claim limit (can goes up to 2.5mil per policy year)

– Riders can be added to cover deductible and cover up to 95% of the total hospitalisation bill

As per the image above, integrated shield plan and medishield life are complimenting each other and its mutually inclusive.

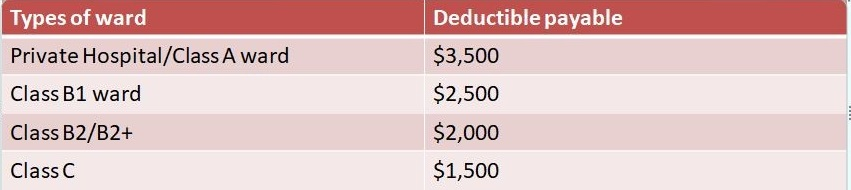

An IP without rider will require individual to pay a 10% co-insurance as well as deductibles. Here is a chart for easy references on deducible payable.

(Annual deductible for Life Assured age 80 years and below next birthday):

Now, let’s take this case scenario as an example.

Mr A, age 45, got warded in a private hospital and incurred a hospital bill of $100,000. He has an IP plan without rider and got to pay a deductible of $3,500 and a co insurance of 10% ($9,650). Amount he needs to fork out is $13,150 and amount claimable by IP is $86,850.

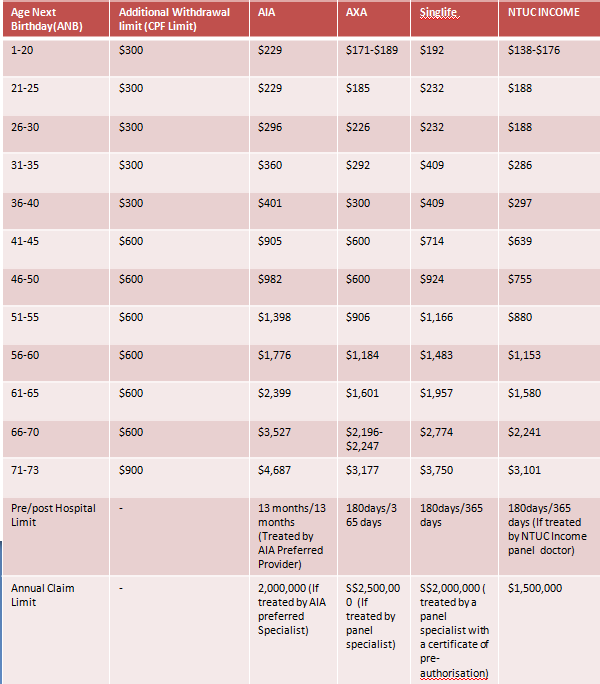

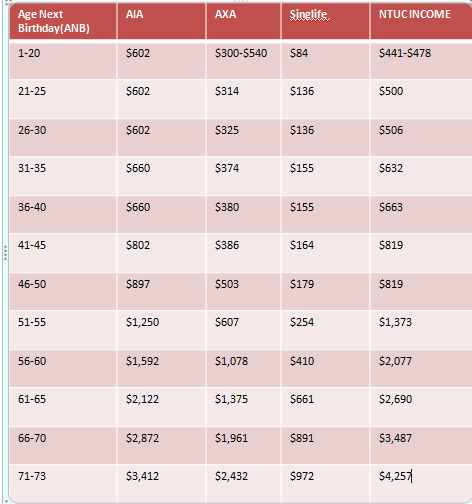

The primary purpose of adding a rider to IP’s main plan is to reduce out of pocket expenses with the exception of a 5% co-payment to be borne by the insured. Below is a table of comparison of premium of rider for Private Hospital from the various insurance companies for references. Payment of rider is only payable via cash.

Here is a general example of how adding rider to a main plan helps to reduce cash payable by life insured.

Mr A, age 45, got warded in a private hospital and incurred a hospital bill of $100,000.

Scenario 1: If Mr A seeks treatment via panel doctor:

He has an IP plan with a rider, amount he needs to fork out is $3,000 (5% co-payment caps at $3000) and amount claimable by IP is $97,000.

Scenario 2: If Mr A seeks treatment via non panel doctor:

He has an IP plan with a rider, amount he needs to fork out is $5,000 (5% co-payment, no caps) and amount claimable by IP is $95,000.

In conclusion, IPs can be used to protect your assets from draining away from paying excessive medical bills. Let us help you compare the right type of coverage across 8 insurance companies by filling the form below