If you’re wondering if Medishield Life itself is sufficient for hospitalisation coverage and what is the best hospitalisation shield plan…

Greetings, readers in Singapore! Today, we are embarking on a journey to delve into the world of non-cancer drug list (non-CDL) coverage provided by various Shield Plans. Whether you are contemplating a switch to a new plan or simply seeking information on available options, this article will offer a comprehensive comparison of non-cancer drug list coverage within different Shield Plans. So, let’s kick things off!

Are you well-acquainted with Integrated Shield Plans (IPs)? They have gained significant popularity because they extend coverage beyond the fundamental MediShield Life (MSHL) plan provided by the government. IPs encompass a broad spectrum of hospitalization expenses, including inpatient treatments, day surgeries, and select outpatient treatments.

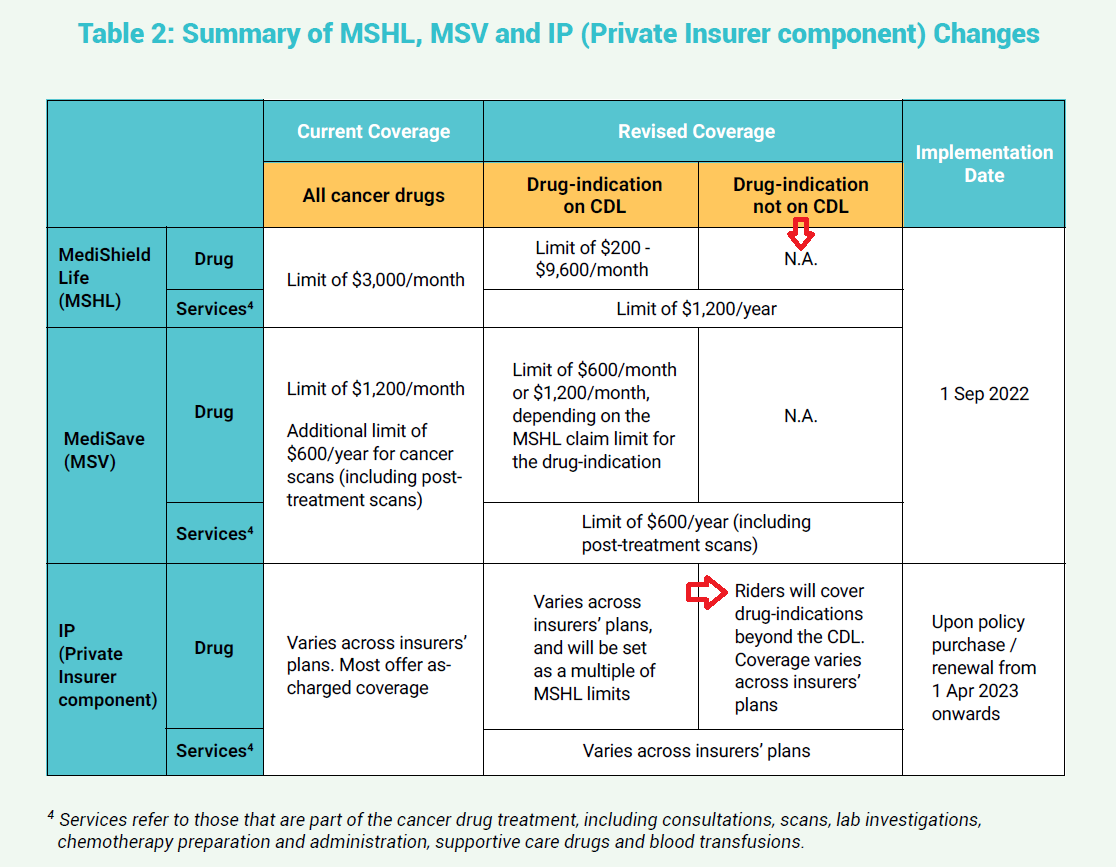

Starting from September 1, 2022, MSHL will limit its coverage to treatments listed in the Cancer Drug List (CDL). This change has been prompted by the escalating costs of non-CDL treatments, which, in turn, have led to higher premiums for both IPs and MSHL.

The policy regarding outpatient cancer treatment benefits has undergone noteworthy changes that warrant your attention. Commencing on April 1, 2023, two fresh benefits will replace the former policy. These new benefits comprise the Cancer Drug Treatment benefit and the Cancer Drug Services benefit. Here is what you need to know:

For most IPs, this modification will take effect on 1st April 2023. Treatments that are not precisely in accordance with the CDL specifications will be non-claimable.

This implies that if you require coverage for non-CDL treatments, it becomes necessary to secure an IP rider. An IP rider serves as an additional insurance policy offering expanded coverage for treatments not included in MSHL or the basic IP plans.

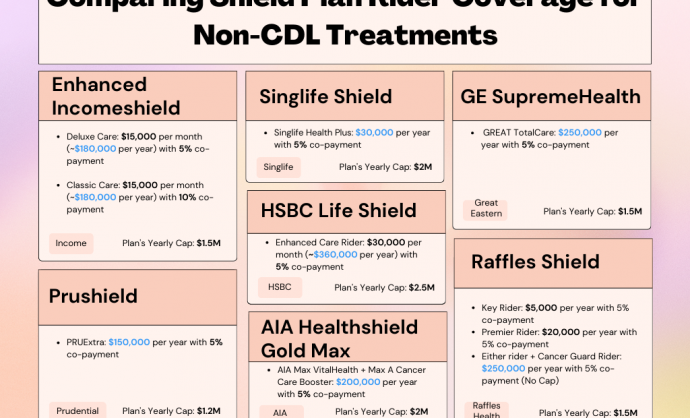

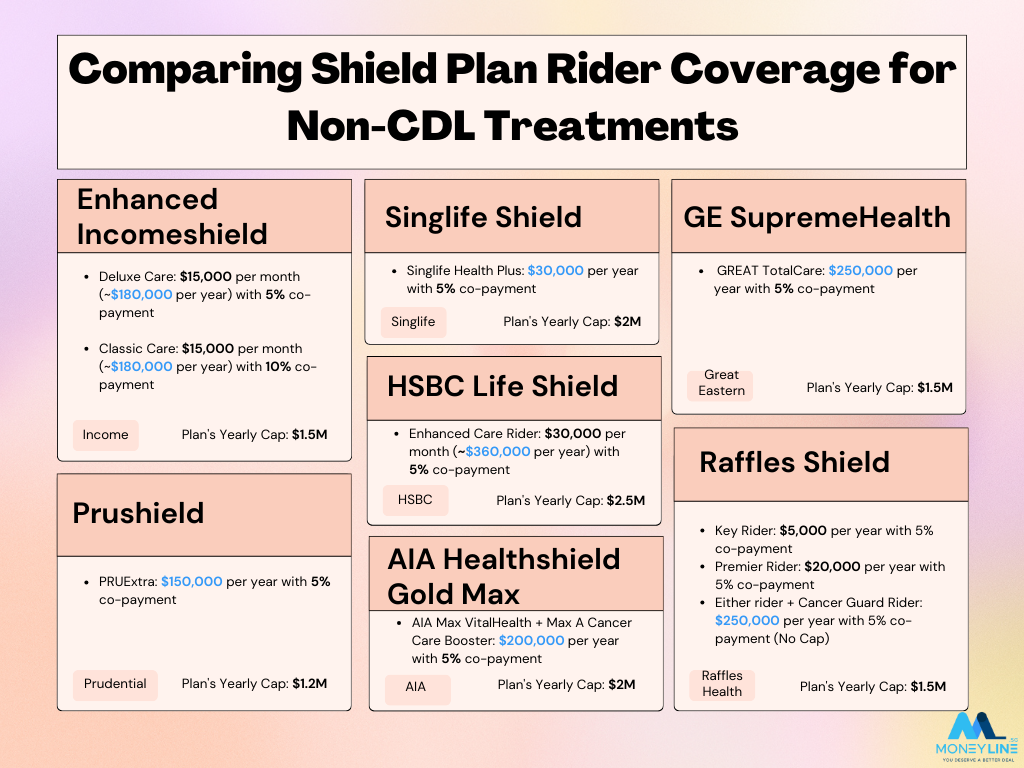

Various insurers offer a selection of IP rider options, each with its unique features. These include Enhanced IncomeShield with riders, Singlife Shield with riders, GE SupremeHealth with rider, Prushield with rider, AIA Healthshield Goldmax with rider, Raffles Shield with riders, and HSBC Life Shield with Enhanced Care Rider. These plans come with varying annual limits, ranging from $30,000 to $360,000 per year, along with diverse co-payment percentages.

Here are some insurers’ IP rider coverage options for non-CDL treatments that can give you an idea of what to expect:

When selecting an Integrated Shield Plan, it’s crucial to scrutinize the coverage for non-cancer drugs list. Keep in mind that different insurers have varying limits on outpatient non-CDL treatments, so it’s advisable to consult your insurer to comprehend their coverage and constraints.

While you can typically find this information on your insurer’s website, it’s essential to note that the details may change due to the dynamic nature of Integrated Shield Plans and MediShield Life coverage. Stay informed to make the best decisions for yourself and your loved ones!

Singapore’s healthcare system has experienced significant transformations in recent years. Staying well-informed about your insurance coverage is vital to ensure that it aligns with your current healthcare needs and financial capabilities.

Although these changes may seem complex, they aim to ensure that every Singaporean has access to crucial healthcare treatments, particularly for cancer. The government acknowledges that cancer treatment can be financially demanding. They have increased coverage for cancer treatments under MediShield Life and MediSave, allowing cancer patients to access more advanced and effective treatments at reduced costs, encompassing targeted and immunotherapy treatments.

However, not all cancer treatments are covered under the Cancer Drug List. This is where IP riders come into play. IP riders offer supplementary coverage for Non-CDL Treatment, which includes cancer treatments not listed in the Cancer Drug List, such as surgery, radiotherapy, and chemotherapy.

In Singapore, there are several options available for covering the costs associated with cancer treatment. These options include:

When selecting a cancer insurance plan, carefully review the policy’s terms, including coverage limits, waiting periods, and exclusions. Compare premiums and benefits across plans to identify the best option that aligns with your specific needs and budget.

IP rider costs can vary, so it’s important to choose one that fits within your budget while ensuring adequate coverage. Prior to making a decision, thoroughly review the insurer’s limits and co-payment percentages.

Despite the initial complexity, the changes in healthcare insurance coverage have been implemented to make sure that everyone in Singapore can access crucial healthcare treatments, especially for cancer. To ensure your insurance aligns with your healthcare needs and budget, stay informed and periodically reevaluate it.

To wrap things up, the Integrated Shield Plan (IPs) has undergone major changes that will impact your coverage. This means that most basic IP plan will now only cover treatments listed under the Cancer Drug List. So if you need Non-CDL Treatment, you might want to consider getting an IP rider.

Remember, it’s important to regularly review your insurance coverage to make sure it fits your healthcare needs and budget.

If you have any questions or concerns, feel free to reach out to us for more information. We’re here to help you navigate the changes and make the best decisions for your health and well-being!

Comments are closed.

3 Comments