In this blog, we will compare and contrast to help you make an informed decision.…

Without a doubt, buying a home in Singapore is a huge financial milestone, and with it comes the question of insurance. In this situation, a crucial question arises: Mortgage insurance vs term insurance – which one is the right choice for you? Don’t stress – we’re breaking it down to help you confidently protect your investment and your family’s future.

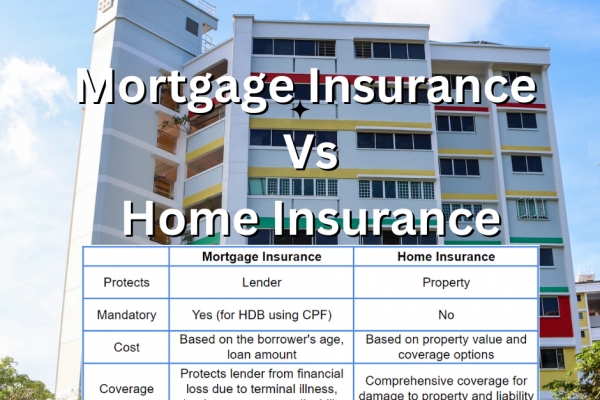

Mortgage insurance is a type of insurance designed to protect your lender (the bank) in case you can no longer make your mortgage payments due to death, disability, or sometimes other circumstances.

Two Main Types: Let’s break down the two primary types of mortgage insurance:

Home Protection Scheme (HPS): In Singapore, if you use CPF funds for your mortgage, HPS is mandatory. It covers your outstanding mortgage balance in case of death or total and permanent disability.

Private Mortgage Insurance: Offered by insurance companies, these policies can provide broader coverage options. Some might also cover situations like job loss or critical illness, depending on the policy specifics.

While HPS is the mandatory baseline for most CPF users, private mortgage insurance can either replace HPS or add a layer of protection and customization to your financial safety net.

P.S. Keep in mind, with HPS, the payout goes directly to your lender to cover your mortgage, not to your family!

Term life insurance is a life insurance policywith coverage for a set period, like 10, 20, or 30 years. In contrast to mortgage insurance, if you pass away during that term, your beneficiaries get a lump-sum payout. Specifically, this money can be used for anything – paying off the mortgage, covering living expenses, your kids’ education, or whatever your family needs most.

Let’s get into the nitty-gritty:

| Feature | Mortgage Insurance (HPS) | Term Life Insurance |

|---|---|---|

| Coverage | Outstanding mortgage debt (reducing) | Chosen amount (fixed) |

| Payout goes to | Lender | Your beneficiaries |

| Cost | Can be paid with CPF | Varies by provider |

| Flexibility | Limited | Highly adaptable |

| Medical Exam | Not required | May be required |

Let’s say you have a mortgage. With mortgage insurance, the payout is limited to your remaining loan amount. Over time, as you repay the mortgage, this coverage decreases.

Term life insurance gives you more control. You could choose policy to only cover the mortgage, OR a larger amount to ensure your family can maintain their lifestyle after you’re gone.

Let’s imagine you take out a $500,000 mortgage with a 25-year repayment period. Here’s how mortgage insurance and term life insurance might play out over time:

| Year | Outstanding Mortgage Balance | Mortgage Insurance (HPS) Payout | Term Life Insurance Payout ($500,000 policy) |

|---|---|---|---|

| Year 1 | $480,000 | $480,000 | $500,000 |

| Year 10 | $350,000 | $350,000 | $500,000 |

| Year 20 | $180,000 | $180,000 | $500,000 |

Let’s say the unthinkable happens in Year 10, and sadly you pass away.

Term life insurance goes beyond simply covering your mortgage, it offers financial support for your family’s overall well-being. To see how mortgage insurance might work for you, check out our in-depth mortgage guide.

The cost (premium) depends on factors like:

Choosing between mortgage insurance and term life insurance depends on your specific needs and priorities. Here’s a breakdown to help you decide:

Basic Mortgage Coverage with CPF Usage:

On the one hand, if you’re using CPF funds for your down payment or mortgage installments, then Mortgage Insurance in the form of HPS is preferred. It offers a basic safety net for your outstanding loan but doesn’t provide flexibility for your family.

Flexibility and Family Protection:

On the one hand, if you prioritize flexibility and want to ensure your family’s financial security beyond just the mortgage, then Term Life Insurance is the way to go. You can choose a coverage amount that surpasses your remaining loan to provide additional support for your loved ones.

Here’s a quick flowchart to visualize your options:

Using CPF for housing?

|

Yes --> Mortgage Insurance (Mandatory)

|

No -->

|

Do you prioritize flexibility and family protection beyond just the mortgage?

|

Yes --> Term Life Insurance

|

No --> Consider Mortgage Reducing InsuranceHere’s a general summary:

This is a general guideline. Consider consulting a qualified financial advisor for personalized advice tailored to your financial situation and goals. They can help you assess your risk tolerance, budget, and future needs to recommend the most suitable insurance combination.

Even if mortgage insurance is mandatory, that doesn’t mean you can’t layer on a term life insurance policy for extra security. This combo can be a smart play, giving your family options if something were to happen to you.

Understanding mortgage insurance vs term insurance is key to making an informed decision for your Singapore home purchase. Don’t be afraid to consult a financial advisor for personalized advice tailored to your financial goals. After all, informed choices lead to greater peace of mind!

If you have a term life insurance policy or a mortgage insurance policy that meets specific requirements, you can apply for an exemption from the Home Protection Scheme (HPS). Be sure to check the criteria on the CPF website or speak to a financial advisor for more details.

Get a personalized comparison – Contact us today!