In Singapore, mortgage insurance is a type of insurance that protects the lender in the event that the borrower is unable to make their mortgage payments. This insurance is typically required by…

In this blog, we will compare and contrast Mortgage Insurance vs Home Insurance to help you make an informed decision. Buying a home is one of the most significant financial decisions you will ever make. It’s a dream come true for most Singaporeans, but it’s also a long-term commitment that requires careful planning and consideration. One of the things you need to think about is insurance. While there are different types of insurance policies you can get, the two most common types for homeowners are mortgage insurance and home insurance.

Mortgage insurance and Home Protection Scheme (HPS) are two types of insurance that are designed to protect homeowners in Singapore.

To qualify for an exemption from the Home Protection Scheme (HPS), you must have adequate coverage from private insurance policies such as mortgage insurance to cover the outstanding housing loan of your HDB flat. In summary, mortgage insurance and HPS are two types of insurance that provide protection to homeowners in Singapore. While mortgage insurance protects the borrower from financial loss, HPS protects CPF members and their families from the burden of outstanding housing loans in the event of death, terminal illness or permanent incapacity.

Home insurance, also known as homeowner’s insurance, is designed to protect the homeowner from financial loss due to damage or loss of their property.

It’s a comprehensive insurance policy that covers a range of events, including fire, theft, natural disasters, and other types of damage. Home insurance also covers liability, which means that if someone is injured on your property, your insurance policy will cover their medical expenses and other damages.

In Singapore, home insurance is not mandatory, but it’s highly recommended. The cost of home insurance is based on the value of your property and the type of coverage you need. It’s important to note that not all home insurance policies are the same, and you should carefully review the policy details before you purchase a policy.

One of the advantages of home insurance is that it protects the homeowner, not just the lender. It provides peace of mind knowing that your investment is protected from unexpected events. Additionally, home insurance can be customized to meet your specific needs, so you can choose the coverage that’s right for you.

Now that we’ve looked at mortgage insurance and home insurance separately let’s compare and contrast the two types of insurance policies.

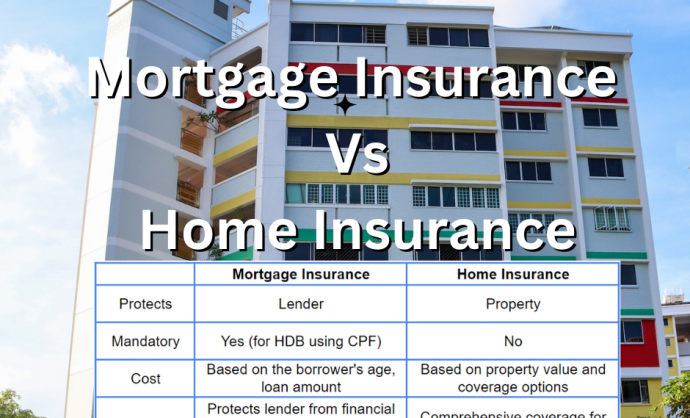

|

Mortgage Insurance

|

Home Insurance | |

| Protects | Lender | Property |

| Mandatory | Yes (for HDB using CPF) | No |

| Cost | Based on the borrower’s age, the loan amount at the point of purchase |

Based on property value and coverage options chosen

|

| Coverage | Protects lender from financial loss due to terminal illness, death, or permanent disability |

Comprehensive coverage for damage to property and liability

|

| Customizable | Yes | Yes |

In conclusion, both mortgage insurance and home insurance serve different purposes in protecting your home and investment in Singapore.

While mortgage insurance protects the lender from financial loss due to default on mortgage payments, home insurance provides comprehensive coverage for your property and liability. It’s essential for homeowners in Singapore to understand the importance of both mortgage insurance and home insurance. By understanding the differences between these two types of insurance policies, you can make an informed decision about the type and level of coverage you need.

Comments are closed.

1 Comment