When it comes to planning for the future, safeguarding our health and well-being should be a top priority. In Singapore, there are various insurance options available to protect ourselves and our loved ones. Two key types of coverage that often come up in discussions are long-term care insurance and health insurance. While both play vital roles in ensuring our financial security, it’s important to understand the differences between the two. In this article, we will explore the distinctions between long-term care insurance and health insurance, helping you make informed decisions about your coverage needs.

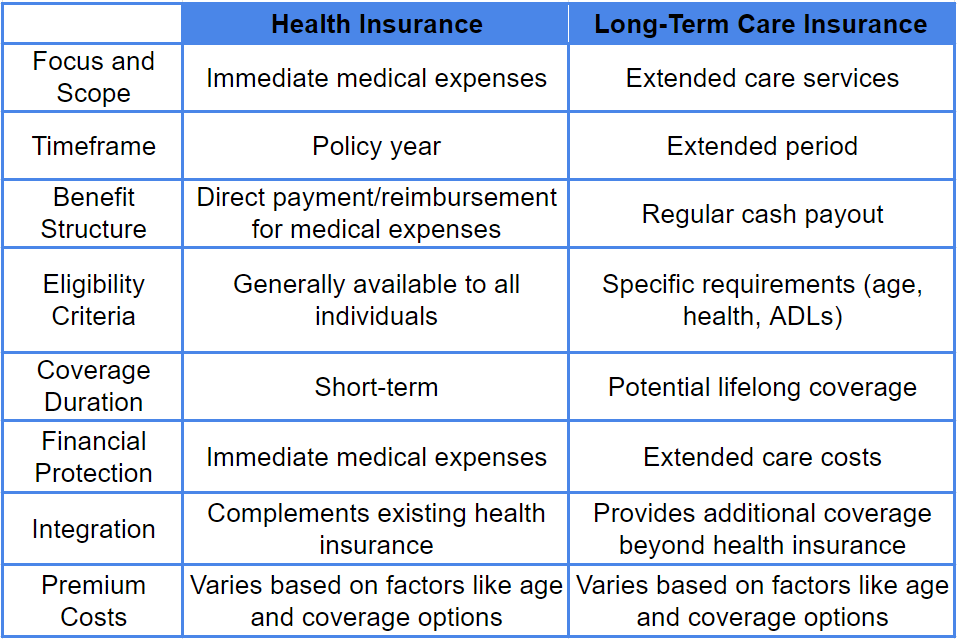

Health insurance is a familiar term to most Singaporeans. It provides coverage for medical expenses, including hospital stays, doctor consultations, surgeries, and prescribed medications.

In essence, health insurance is designed to protect you against unexpected medical costs and provide access to quality healthcare services. This type of insurance typically focuses on acute and short-term medical needs, such as accidents, illnesses, and preventive care.

Health insurance plans in Singapore, such as MediShield Life and Integrated Shield Plans, are essential for managing healthcare expenses. They help offset the costs of hospitalization and certain outpatient treatments, ensuring that you receive the necessary medical attention without depleting your savings. These plans often have deductibles, co-insurance, and annual claim limits, depending on the specific coverage you choose.

While health insurance caters to immediate medical needs, long-term care insurance takes a broader perspective by addressing the potential costs of long-term care services.

Long-term care refers to the assistance required when an individual experiences difficulties in performing daily activities due to aging, illness, or disability. These activities may include bathing, dressing, eating, mobility, and even supervision due to cognitive impairment.

Long-term care insurance provides coverage for the expenses associated with long-term care services, whether received at home, in an assisted living facility, or a nursing home. This type of insurance recognizes that chronic conditions and disabilities may require extended care, which may not be covered by regular health insurance plans.

In Singapore, CareShield Life is a long-term care insurance program introduced to provide Singaporeans with financial support should they require long-term care. It offers a monthly cash payout to policyholders who are unable to perform at least three out of six Activities of Daily Living (ADLs). The cash payout can help cover the costs of caregiving services, home modifications, or residential care, providing individuals with greater peace of mind and financial security.

Now that we’ve explored the basic concepts of health insurance and long-term care insurance, let’s highlight the key differences between the two:

– Health insurance primarily addresses immediate medical expenses, including hospitalization and outpatient treatments.

– Long-term care insurance focuses on providing financial support for extended care services required due to chronic conditions, disabilities, or age-related limitations.

– Health insurance covers medical needs within a specified period, usually a policy year.

– Long-term care insurance considers the potential need for care over an extended period, often for the rest of an individual’s life.

– Health insurance plans typically offer direct payment or reimbursement for medical expenses incurred, up to predetermined limits.

– Long-term care insurance provides a regular cash payout, helping policyholders cover the costs of long-term care services.

– Health insurance is generally available to all individuals, with premiums based on factors such as age, health condition, and coverage options.

– Long-term care insurance eligibility may have specific requirements related to age, health condition, and ability to perform ADLs.

When it comes to choosing the right coverage, it’s crucial to consider your current health status, lifestyle, and long-term goals.

Here are some factors to keep in mind:

Remember, it’s essential to consult with insurance professionals or financial advisors who can provide personalized guidance based on your unique circumstances.

In Singapore, health insurance and long-term care insurance serve different purposes in protecting your health and financial well-being.

Health insurance focuses on covering immediate medical expenses, while long-term care insurance provides coverage for extended care services. Understanding the differences between these two types of insurance is crucial for making informed decisions and ensuring comprehensive coverage.

Assess your current health needs, financial preparedness, and long-term goals to determine the appropriate coverage for your situation. By carefully considering these factors and seeking professional advice, you can create a comprehensive insurance plan that safeguards your health and provides financial security, both in the present and the future.

Comments are closed.

1 Comment