Singaporeans are living longer. Statistics show that 50% of members aged 65 today will live beyond 85. This means that we will be spending more time in retirement and old age. To hedge against this, CPF LIFE was introduced as a “national longevity insurance annuity scheme”. LIFE = Lifelong Income For The Elderly.

This scheme ensures that Singaporeans don’t run out of their retirement savings by providing a monthly payout no matter how long they live, until 70, 80, 90, or 100… or beyond.

Prior to the introduction to CPF LIFE, there has already been an existing scheme: The CPF Retirement Sum Scheme. But if you’re reading this now as someone aged below 64, you will likely be enrolled into CPF LIFE by default.

All three CPF LIFE plans work in the same way.

The premiums are paid from your CPF Retirement Account savings and earn CPF interest rates of up to 6%, which includes the extra interest of up to 2% from the Singapore government. What’s good about this is that the interest rates you earn on the premiums are higher and relatively risk-free.

This interest earned is then pooled, which enables all under CPF LIFE to receive monthly payouts should they be alive, even when their annuity premium gets exhausted. Conversely, this means that if a CPF member dies before their annuity premium is exhausted, he will lose his pooled interest. Basically, CPF LIFE works based on risk-pooling, an insurance mechanism.

But don’t be too worried. If a member passes away before exhausting his annuity premium, whatever the member has contributed into the CPF LIFE scheme (principal amount), less the payouts already given out, will be passed down to his loved ones as a CPF LIFE bequest amount.

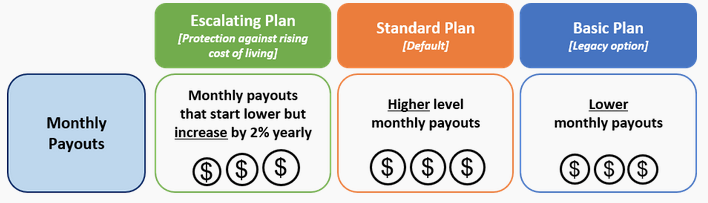

Now that we are clear on how CPF LIFE works, let’s look at some of the CPF LIFE plans. Everyone has a different idea of how they want to retire. Some indulge in pleasures until they’re old, while some don’t mind leading a simple life and live frugally. If you don’t choose your plan, you will automatically be enrolled into the Standard Plan.

As such, CPF Life comes with three different plans to cater to different retirement lifestyles: Escalating Plan, Standard Plan and Basic Plan. Let’s go into each one.

Source: CPF website, CPF LIFE FAQ page

With the Escalating Plan, the monthly payouts starts lower and increase by 2% every year. The bequest amount will be higher in the beginning but falls sharply once the CPF Life member pass 75 years old.

As for the standard plan, it provides higher and leveled payouts at a cost of a lower bequest amount.

The CPF LIFE Basic Plan offers lower monthly leveled payouts but a higher bequest amount to your beneficiary upon your death.

Singapore citizens or PRs who are born on Jan 1, 1958 and after will be enrolled into CPF LIFE automatically.

If you’re older, you can still opt in for CPF LIFE by logging into my CPF Online Services. The cut-off date is 1 month before your 80th birthday.

How much you receive from CPF LIFE will depend on a few factors: gender, age, the LIFE plan you chose, as well as the amount of RA savings you have. Of course, if CPF interest rates and mortality rates in Singapore change, CPF will also adjust the payouts according, determined by actuarial consultants.

Here’s how your payouts might look based on your retirement sum (which is essentially your OA + SA at the age of 55 years old).

| Basic Retirement Sum* | Full Retirement Sum* | |

| Standard Plan | $791 to $870 | $1,440 – $1,588 |

| Escalating Plan^ | $620 to $689^ | $1,133 – $1,260^ |

| Basic Plan | $724 to $799 | $1,314 – $1,452 |

Results computed from CPF LIFE Estimator

*The Basic Retirement Sum is $93,000 in 2021. The Full Retirement Sum is $186,000 in 2021. The sums change about 3% every year due to inflation.

^This is the payout for the first year. It will increase by 2% every year.

This depends on how much you have in your CPF balances, really. If you’re able to hit Full Retirement Sum, which is $186,000 as of 2021, it seems like you will be able to live off an income that can cover basic necessities

But if you only hit Basic Retirement Sum, CPF LIFE monthly payouts alone could be inadequate if you still need to contribute to your household. After all, at the age of 65, some of us might have children who are just going into university, and may even need to support elderly parents.

But, who knows? You may be working well past 65 too. Or, you might want to retire at 40 and travel the world. So, it really depends on how you envision your retirement to be at the point of time when you want to retire.

If you think that CPF LIFE payouts may not be enough, you can supplement your retirement income and don’t wait until you’re 65 to do so!

With your CPF savings, you can start investing with 0% cash upfront. With your OA and SA savings, you can invest in investment products under the CPF Investment Scheme: like unit trusts, endowment policies, exchange traded funds (ETFs), and so on. This can help you grow your savings.

You can also put aside money in retirement plans such as NTUC Gro Retire Ease, Aviva MyRetirement choice and Manulife Retire Ready. Paying a sum of money yearly or monthly for a fixed premium term, you can choose to receive payouts until a certain age.

Of course, you can look into other ways of growing your money, such as investing in property, gold, or even stocks and bonds. Just make sure you do your homework to make each dollar work harder for you.

A common thing that people wonder about is how CPF LIFE compares to private annuity plans. The truth is, CPF LIFE interest rates are relatively risk-free, which means that CPF LIFE provides the one of the highest guaranteed payouts when compared with private annuities.

But private annuities usually have a non-guaranteed component, which means that the overall return could be higher. Note, you can also invest in private annuity plans through the CPF Investment Scheme.

CPF Retirement Sum Scheme is the older “version” of CPF LIFE (they are completely different though). The difference between the new CPF LIFE and the older CPF Retirement Sum Scheme is the duration of payouts.

The previous CPF Retirement Sum Scheme will draw from your CPF Retirement Account and stop when the money is exhausted.

As for CPF LIFE, in order to pay everyone for life, you pay a lump-sum premium from your Retirement Account to CPF LIFE. In other words, it’s an annuity plan, not a simple retirement fund.

You may also want to read: How much do I need to retire in Singapore? in that article, we explain why you may not have to planned for an inflation adjusted stream of income for retirement.

For more information on how you can maximize your CPF LIFE payouts, or how to supplement it for a more comfortable retirement, you can answer the fields below and check to see if you’re eligible for a Free 1 session non-obligatory Financial Consultation with a License Financial Planner.

Comments are closed.

5 Comments