Recently, we post an article about the increasing cost of cancer treatment and how Ministry of Health (MOH) has put a limit on the type of cancer treatment that can be claimed for Integrated Shield Plans.

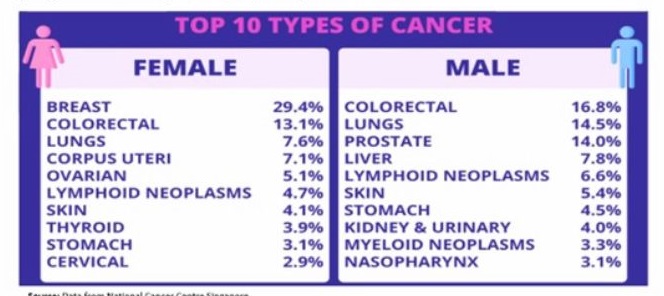

Cancer according to the Ministry of Health is the number one killer in Singapore, even though health insurance (whether medishield life or private health) covers most form of cancer treatment, it is likely that the financial burden of being diagnosed with cancer goes beyond just treatment, as such cancer is not only detrimental to one’s physical health but financial as well.

There are plans in the insurance industry that can be bought to help mitigate the financial burden faced by an individual and their family members caused by cancer.

In this article, we understand the two types of policies mainly cancer and critical illness insurance and explore the pros and cons of getting just cancer insurance vs a critical illness insurance policy.

The core purpose of a CI cover is to pay the insured a lump sum on the diagnosis of any of the ailments listed in the policy document. Though cancer; heart attack; or stroke are part of the insured diseases under critical illness insurance policies, Critical illness insurance in fact covers more than 30 other conditions and it is an important part of financial risk management planning for dealing with various types of severe illnesses. Adequate critical illness coverage will ensure diagnosis are treated and providing pay out to replace a potential loss of income due to the inability to work when critical illness is diagnosed. There are officially 37 critical illness diagnosis defined by the Life Insurance Association which are covered by most insurers. Here are the 37

| 1 Major Cancer

2 Heart Attack of Specified Severity 3 Stroke with Permanent Neurological Deficit 4 Coronary Artery By-pass Surgery 5 End Stage Kidney Failure 6 Irreversible Aplastic Anaemia 7 End Stage Lung Disease 8 End Stage Liver Failure 9 Coma 10 Deafness (Irreversible Loss of Hearing) 11 Open Chest Heart Valve Surgery 12 Irreversible Loss of Speech 13 Major Burns 14 Major Organ / Bone Marrow Transplantation 15 Multiple Sclerosis 16 Muscular Dystrophy 17 Idiopathic Parkinson’s Disease 18 Open Chest Surgery to Aorta |

19 Alzheimer’s Disease / Severe Dementia 20 Fulminant Hepatitis 21 Motor Neurone Disease 22 Primary Pulmonary Hypertension 23 HIV Due to Blood Transfusion and Occupationally Acquired HIV 24 Benign Brain Tumour 25 Severe Encephalitis 26 Severe Bacterial Meningitis 27 Angioplasty & Other Invasive Treatment for Coronary Artery 28 Blindness (Irreversible Loss of Sight) 29 Major Head Trauma 30 Paralysis (Irreversible Loss of Use of Limbs) 31 Terminal Illness 32 Progressive Scleroderma 33 Persistent Vegetative State (Apallic Syndrome) 34 Systemic Lupus Erythematosus with Lupus Nephritis 35 Other Serious Coronary Artery Disease 36 Poliomyelitis 37 Loss of Independent Existence |

A Critical illness insurance policy in Singapore will allow the policy owner to claim on the life insured upon diagnosis of any of the listed critical illness, in addition, most insurers also provide option for early-stage critical illness coverage which makes the definition more lenient for the pay out to be made.

Available critical illness plans

When it comes to the usefulness of critical insurance plans to just specifically cover cancer treatment and related expenses, one major drawback is that such plans maybe expensive and restrictive to a person seeking to get insured. Other than providing coverage for cancer diagnosis, critical illness insurance also priced in coverage for the other critical illnesses as listed above and some even more. While the probability of getting some of the other illnesses are extremely low, the fact that critical illness insurance provides coverage for many other conditions offers a “what if it’s not cancer” wager that brings up the premium as compared to just getting a cancer insurance plan.

Another disadvantage of Critical illness insurance is that it may not provide coverage to client that are diagnosed with certain conditions. Example, if an applicant has a pre-existing moderate/severe heart, nervous system or congenital condition, the applicant may potentially receive a blanket “declined” on his/her critical illness application. This means there will not be any coverage granted at all for cancer even if a pre-existing condition is totally unrelated or have little to no chances of causing cancer.

Cancer insurance typically covers all forms of cancer from early to advance stage and may even cover some form of pre-early cancer conditions. Some of the flaws of critical illness insurance plans can be addressed by Cancer Only Insurance Plans. One of its plus points of cancer insurance the relatively low and affordable premium compared to critical illness insurance. Given that about 70% of critical illness claims are due to cancer, cancer insurance itself is a worthy addition to be included into an individual financial protection portfolio. Generally, a cancer insurance policy provides a partial or lump sum pay-out for treatment and diagnosis of early to advance stage cancer, the plan may include hospitalisation, chemotherapy, radiation, surgery, coverage etc. due to cancer.

Another major benefit of Cancer insurance plan is that there is no requirement to declare pre-existing conditions that are unrelated to cancer. As such, a person can still be considered for cancer insurance coverage even with the presence of a health condition such as diabetes or moderate/severe heart or congenital illnesses. The disregarding of pre-existing illness mechanism, unlike critical illness insurance, allows a person to still receive protection payout even with other pre existing conditions in the event of a cancer diagnosis to relieve further financial burden if cancer occurs.

Cancer insurance as it stands only provides coverage for cancer, this overlooked a lot of potentially fatal but insurable conditions which a critical illness insurance plan can provide. While statistic shows the high concentration of claims on cancer diagnosis, there are always the probability of other illnesses getting diagnosed. Several conditions such as heart attack, liver failure, kidney failure and stroke are also commonly claimed upon and can result in the destruction of a person’s livelihood as well as affecting ones’ financial capability to sustain his/her family lifestyle and necessities if not covered for. A cancer insurance must therefore not be the only illness insurance one should have but a compliment to a proper critical illness insurance policy.

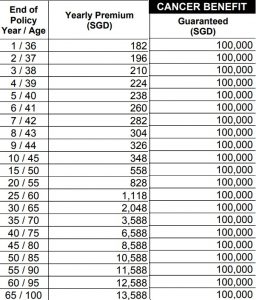

Another downside of Cancer insurance is the steep increase in premium from a certain age onwards especially if the plan is renewable. There are a wide range of option on the policy term of cancer insurance with most having a renewable option that can be yearly renewed or upon every 5 to 10 years of policy term. This results in an ever-increasing premium unlike a critical illness policy where you can decide on the coverage term to be covered for and have a fixed yearly premium to be paid and protect you to until a designated age. This may ultimately lead to a point where the premiums may be unsustainable given that the coverage itself may be lower than the premiums paid even if you bought the plan at a younger age.

While a cancer insurance is an essential financial tool to help protect against the financial burden of a cancer scare, a proper critical illness insurance is still crucial to give you that assurance in case life decide to throw you a different hurdle to overcome. A cancer insurance can act as a compliment to your insurance portfolio coverage, but it can never be the only coverage you should have in the arsenal of health and income replacement products.

Providing adequate and affordable life insurance coverage is an important deterrence to any financial shock that one may face upon any unfortunate health or life events. A Proper financial portfolio should prepare you against any eventualities.

If the policyholder gets diagnosed with a condition of a defined clause, a certain percentage of the sum assured or even the full amount is paid out (subject to applicable limits depending on severity). There is usually 90 days waiting period after the policy’s acceptance before any condition diagnosed can be claimable.

Certain policies offer free regular health check for the insured throughout the entire policy period.

Let a licensed financial representative provide you with insights to over 10 insurers companies critical illness and cancer insurance policies. Comparison will be done based on your objective, time horizon and budget to ensure you get the best option available.

Disclaimer : Moneyline.SG does not endorse, rate or recommend any particular insurer or insurance product offered by an insurer. All info provided do not take into account your financial objective, needs and budget.

Comments are closed.

2 Comments