CPF Nomination: Nomination for the Central Provident Fund (CPF) is an important essential to have for all every citizen. Signing up for a Will and leaving behind a Legacy is equally as important, if not more.

Have you come across the term “CPF Nomination” in your life? If yes, what do you know about it? And if no, ever wonder why it’s a topic that needs to be discussed?

The scheme allows the Government to quickly allocate CPF funds to the next of kin (or other nominated beneficiaries) when a member dies. If a person wishes his or her CPF to go to someone else after death, he or she must make a nomination during life. By default, the nominee will receive the money in cash (via cheque or GIRO). You can also choose to have your nominee receive your CPF savings, unused premiums for the CPF LIFE annuity, and discounted Singtel shares.

According to CPF Board, “The Central Provident Fund (CPF) is a compulsory comprehensive savings plan for working Singaporeans and permanent residents primarily to fund their retirement, healthcare and housing needs.”

Hence, it is a form of compulsory saving for your retirement. However, what if you pass away before retirement age? For example, you have just turned 50 and passed away unexpectedly due to a fatal accident. What will happen to all your savings in the CPF account?

This is when CPF Nomination comes into the picture. Simply put, it is the process whereby you state who should receive your CPF savings upon death.

When you pass away, the CPF monies that you have accumulated will not be automatically transferred to your family members. You need to make sure that your loved ones know about the CPF monies you wish to leave them. You can do this by making a CPF nomination.

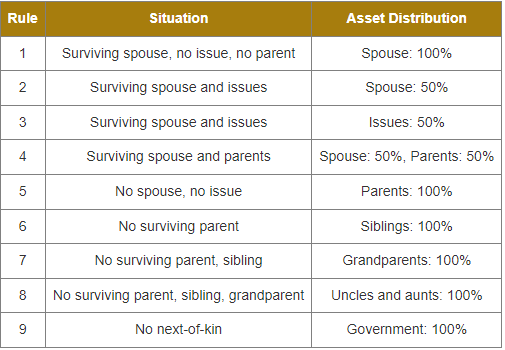

If you fail to nominate your beneficiary for your CPF savings, the savings will be distributed according to the Singapore intestacy laws.

When you die without a will, you die “intestate”. Your estate will be distributed according to intestacy rules.

In most cases, this means that your spouse, parents or children will inherit your estate.

You have a Will. Check.

You have nominated your CPF account upon death to your loved ones. Uncheck.

But, hold it right there.

In this day and age, there are still many who are not aware that one cannot will away one’s CPF monies upon death.

First, it is important to know that when you die, the money in your CPF account does not form part of your estate and cannot be willed away by you. The CPF Board distributes your CPF monies according to the rules set out under the Central Provident Fund Act (chapter 36).

It is important to note that CPF nomination does not replace a will. If you were to pass on with a will and without making a CPF nomination, the Intestate Succession Act would apply and your family members would inherit your CPF monies according to its dictates.

In other words, if you don’t make a will, then the law makes one for you and gives it away according to its own dictation. If there’s something about the way the law distributes your stuff that doesn’t sit well with you, then make sure you make a CPF nomination first before writing this off as an unnecessary exercise.

CPF nomination allows you to choose who receives your CPF savings. It is an important estate planning tool that you should use in conjunction with a Lasting Power of Attorney (LPA) and a Will.

The Public Trustee Office(PTO) will handle the distribution of CPF monies in line with Singapore’s intestacy laws. The PTO will charge an administration fee for the distribution of your savings without a nomination.

This process can take up to 6 months before the administrator determines which family members are entitled to what share of your CPF savings. The PTO deducts an administrative charge on your CPF savings when it distributes the savings to them.

CPF funds cannot be distributed through a Will.

You can make a CPF nomination to make sure that you take care of the special people in your life after your death.

Note: For Muslim members who have not yet made a nomination, their CPF savings will be distributed in accordance with the Administration of Muslim Law Act.

You may do so via my cpf Online Services or at any of the CPF service centres.

You will need 2 witnesses who are at least 21 years old with sound mental capacity, cannot be any of your nominee(s), and are Singpass holders if you are making a CPF nomination online.

Make your nomination any time, and all the time. Just head to the CPF website online.

Don’t forget you can also book an appointment at your CPF Service Centre to make your CPF nomination.

But apart from CPF monies, you will need to have a Will to give away your other assets upon your death. In addition, if you want to exclude certain people from inheriting your other assets in your estate, then a Will is necessary.

A will is a document that sets out what you want to happen to your assets after your death. It includes gifts of money or property, making arrangements for the care of minor children, and appointing an executor to administer your estate.

A person who dies without leaving a valid will dies intestate. Without a will, the rules of intestacy determine how to distribute a person’s assets and property.

Dying without a valid will means you have no say in who inherits your assets. There is also no guarantee that what you want to happen will happen. This can devastate those who are left behind and lead to family disputes

It is a common misconception that only the wealthy need Wills or Trusts. Everyone should have a Will, and in fact, without one, you could be creating more work and expense for your family at a time when they are grieving your loss.

Finishing off, I hope that you’ve learned why it is critical to have a CPF nomination and estate planning. This is an important aspect that people live with their entire lives, and never give much thought to.

Have a question? Contact us to get answers.

Comments are closed.

2 Comments