Annuity Review Singapore - You’ve saved up over $100,000 in the past few years and you want to maximize your…

Annuity Mistake: In Singapore, thousands of people have begun saving for retirement and considering annuities. However, with numerous options available, finding the perfect fit for your needs can be challenging. This guide is here to help you steer clear of three costly annuity mistakes that could save you thousands, and show you how to avoid them.

But annuities are more complex than they appear. There are many varieties and types to choose from, and each offers different benefits, drawbacks and costs.

The first mistake is not buying an annuity plan through Supplementary Retirement Scheme (SRS) . The reason is simple – by using SRS to buy an endowment annuity plan, you can enjoy a tax relief of up to $15,300 each year!

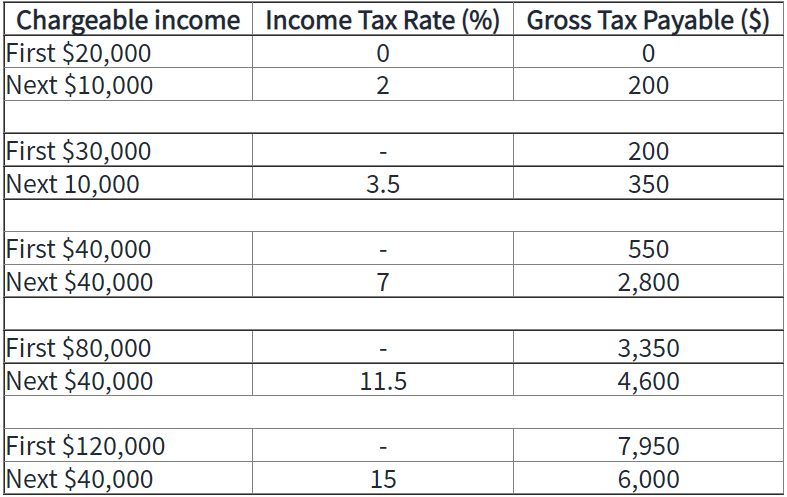

You earn $60,000 a year. Without any tax reliefs, you’ll pay $1,950 in income tax. Here’s how it works.

Meanwhile, if you have contributed the maximum amount of $15,300 to your SRS account, then your taxable income is reduced to $44,700 and you will pay significantly less in taxes.

The SRS is not compulsory, but it offers significant tax benefits.

Taking part in SRS can help you save more than $1,000 on your tax bill!

If you are looking to reduce your chargeable income, tax relief can be a great tool. The amount of tax that you have to pay each year depends on how much income falls into each tax bracket, as detailed in the table below.

The current SRS contribution limit stands at S$15,300 per year – and any amount contributed will be eligible for tax relief up to the prevailing income tax relief cap of S$80,000. The money in your SRS account can also grow on a tax-deferred basis.

Not using your SRS yearly is a big annuity mistake!

The word “annuity” evokes a feeling of safety for most investors. It conjures up images of a guaranteed income stream that will last as long as you do, a modest monthly benefit that can be counted on until that final day has come.

You may be tempted to buy an annuity from the first insurance company that offers one. But before you commit to a purchase, shop around to see whether someone else might offer better terms. You can find out more about different types of annuities by reviewing their Policy Illustration and comparing them with similar products. Also, consider the financial strength of the insurance companies that offer each annuity; choose one that’s likely to stay in business as long as you own your annuity — don’t make such mistake with your long-term annuity!

When shopping for an annuity, it’s important to compare rates in the marketplace. Rates can vary as much as 2-3% in the same category, so you need to make sure you’re getting the best rate possible for your situation. This will make a huge difference when it comes to accumulating money for distribution at retirement age or when you begin receiving income. Even if you’re already retired and drawing income, you can still shop around for better rates by rolling all or part of your existing annuity into another one that pays more.

Some annuity plans may help you live comfortably in retirement, others may leave you struggling to make ends meet. Choosing the wrong plan could cost you thousands in fees and lost opportunities, so it’s important to understand the risks before making a decision.

If you need money from your annuity before it matures, cashing it out early may be a big mistake, depending on the type of annuity you have. Some annuities have surrender periods that last several years. A surrender charge can be as high as 40% of your principal in the first year, and decreases each year until it’s gone.

If you prefer not to wait for your money until the surrender period ends, you can borrow from your annuity. Borrowing from your annuity will result in interest charges and administrative fees, but there won’t be any penalties if you repay the loan according to its terms. If your annuity allows for it, you can also make partial withdrawals without penalties, although this will reduce the amount available for your retirement as you’ll be withdrawing some of it early.

The best time to buy an annuity is when you are young and have time on your side. With age, the annuity’s income potential from your savings diminishes. This mirrors the way CPF contributions begin as soon as an individual starts working.

If you wait too long before purchasing an annuity, you could commit a mistake that potentially lose thousands of dollars.

The number of years you have left before retirement will reduce the returns from annuity income. For example, if you were age 40 and purchased an annuity with a $50,000 premiums ($10,000 premium for 5 years) and a 10-year payout period, then waited until age 60 to begin receiving payments, your total monthly income would only be about $122,000.

As another example, consider someone who is age 50 and purchases the same $50,000 annuity with a 10-year payout period. If this person waits until age 60 before beginning (which is typical), then he or she could expect about $75,000 in total monthly income. This is because the insurance company has fewer years remaining to pay out its investment returns if it issued it at a later date.

If you start off your $50,000 annuity is by 10 years later, you can easily lose out on $47,000 ($122,000 – $75,000)

Regardless of where you are in life, it’s important to think through the decisions that you make and learn as much as you can about the products and services you purchase, and avoid any annuity mistake. If an annuity is something that may interest you, understanding its terms, risks and limits—and the way they will impact your future—is the way to go.

Answer your annuity questions (annuity may not be for everyone, but it could help you save money)!

Comments are closed.

1 Comment