Careshield Life Supplement: Best Upgrade Option & Comparison We Compare over 15 Life insurers to get you the best Careshield Supplement insurance plan in Singapore Learn about…

We have all heard it, Careshield life will kick-in in 2020 whether we like it or not. Unlike its predecessor, Careshield Life will no longer be optional, all Singaporeans and PR age 30 and above from 2020 onwards will automatically be enrolled into the scheme. The purpose of careshield life is to provide a monthly income in the event the insured suffers from severe disability. The current definition for severe disability is the inability to do 3 out of the following 6 Activities of Daily Living (ADLs)

If you can think well enough, Careshield Life is still not an all in one solution to your protection needs.

Read How Much Should I Spend On Insurance

If you are born from 1980 onwards, you are automatically enrolled into Careshield Life, this means for those who turned 40 in 2020, you will no longer be eligible for Eldershield and Careshield Life will be your default and compulsory coverage as a national severe disability income plan.

Unlike Eldershield, those who turn 30 years old from 2020 onwards will automatically be included in the Careshield Life scheme, you will not be able to opt-out of it just like your MedishieldLife.

Existing Eldershield carriers born in 1979 and earlier, whom are not severely disabled, will have the option to switch to Careshield Life, this is optional as those who prefer to stick to their Eldershield plan will get to keep it. For those born between 1970 to 1979 and are not severely disabled, you will be automatically transitioned to CareShield Life in 2021. This is the only group that will be able to opt out of CareShield Life and have the premium difference fully refunded to them.

There will be more information on the premium and the procedure to switch as we move close to the implementation date (we will provide an update once the details are clearer).

As Careshield Life is a much-improved version of the Eldershield Plan, it is foreseeable that it will come at a higher cost. Just like its predecessor, Careshield Life will cost slightly higher for women than it is for men. Starting premium for a male at age 30 will be $206/year and premium for 30 years old female will start at $253/year. In contrast, Eldershield starts at $175/year for male and $218/yr for female at age 40.

The premium for Eldershield are payable till age 65 whereas the premium for Careshield Life will consist of 38 payments of which the earliest one will stop paying is till age 67.

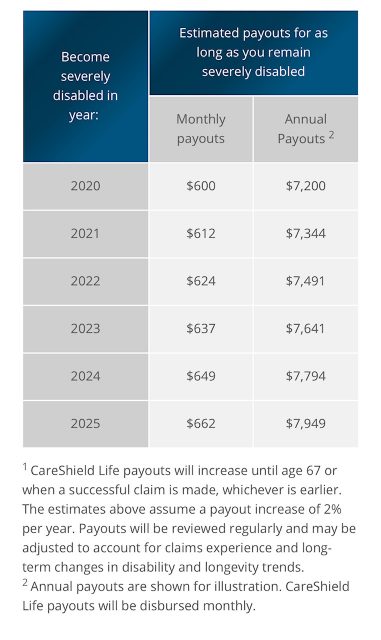

Careshield Life will pay at least a basic sum assured of $600/mth for as long as care is needed; this is a slight improvement from Eldershield which only pays $400/mth for up to 6 years.

There is also an escalated payout feature for Careshield Life estimated at 2% p.a. However, the government has indicated that its payout feature will be review periodically to account for claim experience and longevity trends.

While premium is set to rise in order to accommodate for a longer payout period, higher sum assured and an escalated payout feature, Medisave will continue to be used to fully fund for the Careshield Life Scheme. For a start, those who qualify will receive permanent subsidies of 20% to 30% and additional support will also be given to those who still cannot afford the premiums.

An announcement will be made closer to the implementation and we will provide an update once the details are clearer

While there is no confirmation if the government will allow insurers to provide supplementary coverage, there have been on-going rumours that at least 5 insurers are vying to provide optional CareShield Life Supplement to individuals who wish to enhance their coverage. Just like its predecessor, CareShield Life Supplement may likely be fundable by Medisave to a certain withdrawal limit, and for those who wish to enhance it even further may pay cash in excess of the limit to fund the supplement.

Do note that this is hypothetical as there hasn’t been any official announcement by any insurers yet to provide Careshield Life Supplementary coverage.

If you are concern about giving yourself adequate protection due to partial or total disability, you may consider getting disability income insurance. Disability income insurance is an occupation centric coverage that provides a monthly income should an individual be unable to carry out his own occupation within a period of time. Fill in your details below and upon your request, a licensed financial planner will draft you a customized plan based on the information you have communicated.

Comments are closed.

3 Comments