Read, Compare, Save! Because You Simply Deserve The Best! Compare Insurances

Just entered into a new life stage and planning your finances to see how you can own your first HDB? Then this is definitely the article that you got to check out because it will help you save time and effort from navigating the cumbersome HDB website to find the right grants/schemes. We have got every HDB grants and scheme right here for you, in a single guide!

Everyone knows that you got to make a down payment when you commit to buying a HDB. Depending on whether you are taking a HDB or bank loan, the down payment amount will either be 10% (HDB loan) or 25% (bank loan) of the HDB valuation. But did you know that you can choose to pay your down payment in two separate instalments? With the Staggered Down Payment Scheme, half of the down payment will be made upon signing of the Agreement for Lease. The other half will be payable when you collect your keys. This lets you delay the down payment amount to 3-4 years later.

If you are a full-time student, NSF or just completed either of those in the last 12 months, here’s a “scheme” that you would want to know.

To encourage young couples who might not have the financial ability (yet) to apply for their own HDB, the Deferred Income Assessment Scheme was introduced in 2018. This scheme is most suited for young couples who are looking to purchase BTOs or uncompleted SBFs because the income assessment is deferred till 3 months before flat completion.

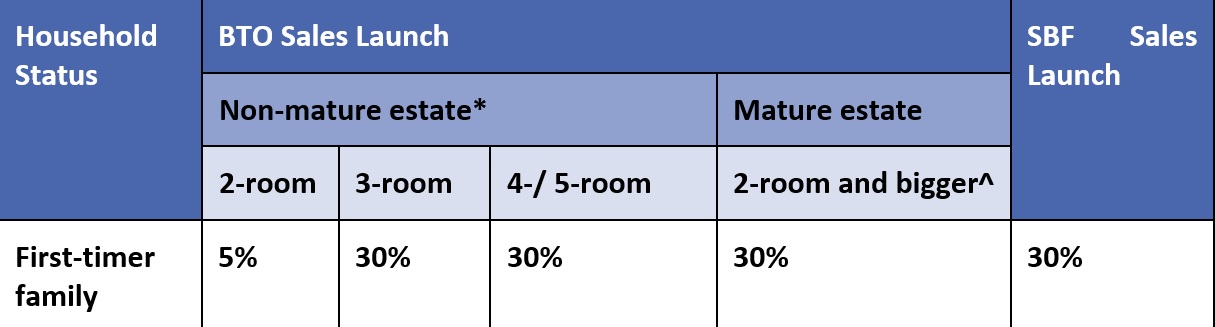

Did you know that you get extra ballot chances if you apply for an HDB as a couple with a child? According to HDB, up to 30% of BTO units and 50% of SBF units are allocated to applicants under this scheme. Here’s how it works.

You will be part of a balloting pool that consists of only couples applying under the Parenthood Priority Scheme. If you fail to secure a ballot number in this pool, you will automatically be eligible for another chance of balloting in the normal balloting pool.

Another child priority scheme that is meant to help families with children boost your chance of an HDB flat is the Third Child Priority Scheme. The most important condition that you need to fulfil? You need to have at least 3 children.

Under the Third Child Priority Scheme, up to 5% of BTO and/or SBF units will be up for balloting for this group of applicants. You will still be eligible for the Parenthood Priority Scheme if you didn’t manage to get a ballot number under this scheme.

Note: This scheme takes priority over the Parenthood Priority Scheme.

With an increasingly ageing population, the government has been looking at ways to help family units stay close together so that there is adequate care and support for parents. One of the solution was the Married Child Priority Scheme, which was introduced to encourage couples to stay close to their parents.

In order to qualify for this scheme, you need to be applying for a flat that is within 4km from where your parents are staying. If your parents have multiple properties, the one which they reside in will be considered for measurement of proximity. Under this scheme, up to 30% of BTO and/or SBF units will be up for balloting for first-timer families.

For couples who are looking to stay with your parents, here’s another scheme that you can consider: Multi-Generation Priority Scheme. The aim of this scheme is to help the married couple and parents get new flats in the same area. Both you and your parents can make a joint application for 2 flats in the same BTO project.

However, the caveat for this scheme is that your parents can only apply for a 2-room Flexi or 3-room flat. Thus, you and your parents can only apply in areas where there are 2-room Flexi or 3-room flat offerings in the new BTO project. This would be suitable if your parents are looking to downgrade their HDB flat to unlock some cash value for retirement.

Applying for the Multi-Generation Priority Scheme will get you 3 ballot numbers: 1 under this scheme and 2 under the normal public scheme.

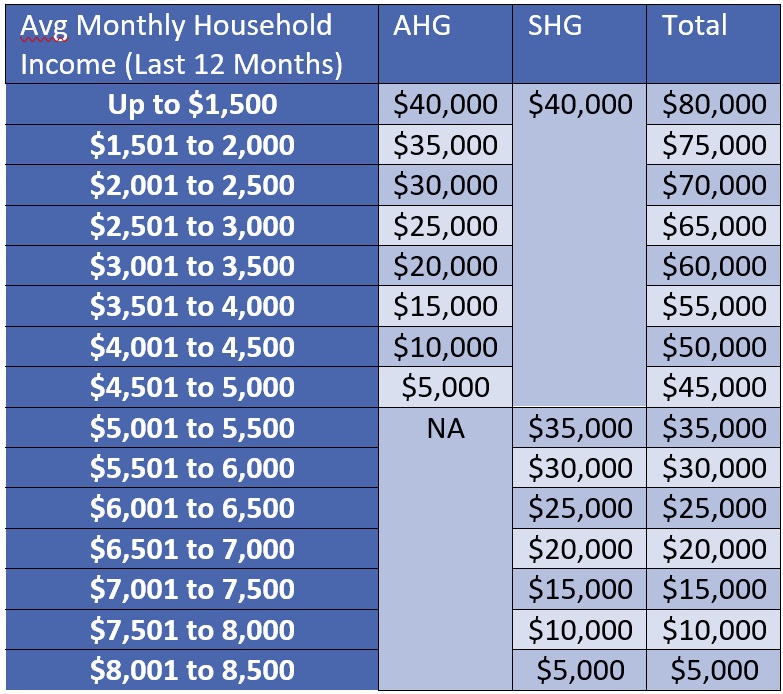

For couples who are first-time owners and have a combined household income of below $5,000, this will be music to your ears. You can receive up to $40,000 in Additional CPF HDB Grants, depending on your actual income level. The grant will be offset from the price that you have to pay on your HDB.

Besides the Additional CPF Housing Grant (AHG), another grant that you should know about is the Special CPF Housing Grant (SHG). This grant is meant for couples who apply for a 4-room flat (or smaller) in a non-mature estate. Similar to AHG, you can receive up to $40,000 in grant to offset from your HDB sale price. If you and your spouse do not mind living in a non-mature estate, this grant is definitely something you should apply for during your flat booking appointment.

Source: HDB

If you are lamenting why most of the grants and priority schemes apply only for BTO units, here’s some good news for you. If you are planning to buy a resale unit or apply for an Executive Condo (EC), there is also housing grant available for you: CPF Housing Grant.

For resale flats, the CPF Housing Grant is $50,000 for 4-room flats (or smaller) and $40,000 for 5-room flats (or larger). For ECs, the CPF Housing Grant is capped at $30,000 if your monthly household income is below $10,000. The CPF Housing Grant reduces $10,000 for every additional $1,000 monthly household income that you earn.

Note: This grant can be stacked together with the Additional Housing Grant (AHG) if your average monthly household income falls below the $5,000 mark.

If you are eligible for the Married Child Priority Scheme or Multi-Generation Priority Scheme, you will automatically be considered for the Proximity Housing Grant (PHG). The only criterion that you need to fulfil is that you need to stay within 4km of where your parents are staying.

Note: The Proximity Housing Grant (PHG) can be stacked with the CPF Housing Grant and Additional Housing Grant (AHG) to help make your home more affordable.

Now that you have a clearer idea of the HDB grants/schemes available to you, it’s time to apply for your first home. Here are some useful resources that will help you in your journey to become a proud homeowner:

Comments are closed.

1 Comment