With more than 70% of Singaporeans being a homeowner, many of us have a home loan to service. It…

Have some cash to spare and not sure where to park it? Well, we have an idea: Safe Financial Product. But not just any products. There are many different plans out there that offer some interesting value proposition for those with cash to spare.

Recently, SingLife, Gigantiq And Dash EasyEarn have been in the limelight for their insurance savings plan that offer good returns with great flexibility. But they are not the only good ones out there. There is one particular plan that will really boost your returns and we are going to show that to you in this article.

But first, let us learn more about the 3 contenders that are enjoying the limelight: SingLife, Gigantiq And Dash EasyEarn

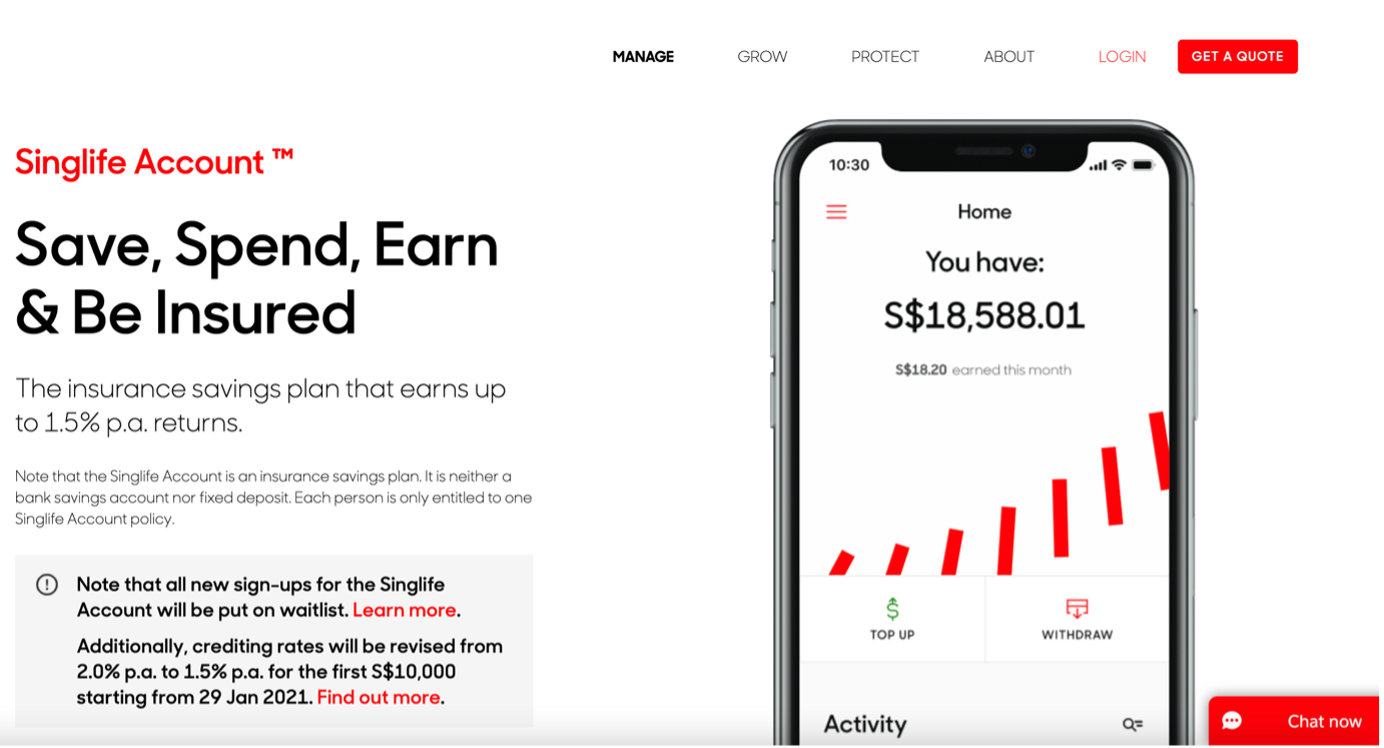

Singlife Account is an insurance savings plan that lets you earn up to 1.5% p.a. returns on your savings. All you need to do is to keep at least $500 in the account and you can start earning interest on your savings without any restrictions.

One interesting feature that comes with the SingLife Account is that you will have your own SingLife Visa debit card. Insurance savings plan don’t typically come with a debit card. You can only get your money at maturity, which can be a few years down the road. But with SingLife Account, the debit card lets you spend whenever you want.

Interest Rate: Up to 1.5% p.a. on the first $10,000; Up to 1% p.a. on the next $90,000

Additional Bonus: 0.5% p.a. when you spend $500 on your SingLife Visa debit card

Minimum Premium: $500

Maximum Account Value: $100,000

Top-Up Available?: Yes

Requirement: Singlife app

Who’s Eligible: Singapore citizen, PR or Work Pass holder, between 18 and 75 years old

GIGANTIQ is the successor of the previously popular Elastiq, which was also offered by eTiQa. It is a single premium, yearly renewable, non-participating universal life plan that offers financial flexibility together with opportunity for wealth accumulation and the assurance of life insurance coverage (i.e. death benefit).

In short, GIGANTIQ is an all-in-one insurance savings plan with optional protection riders to fulfil your life goals.

Interest Rate: 1.8% p.a. on the first $10,000; 1% p.a. on anything above $10,000

Additional Bonus: 0.25% p.a. when you purchase additional protection plans with eTiQa

Minimum Premium: $50

Maximum Account Value: None

Top-Up Available?: Yes

Requirement: TiqConnect app

Who’s Eligible: Singapore citizen, PR or foreigner with a valid Work Pass/Permit or Long-Term Visit Pass who are between 17 to 75 (age next birthday)

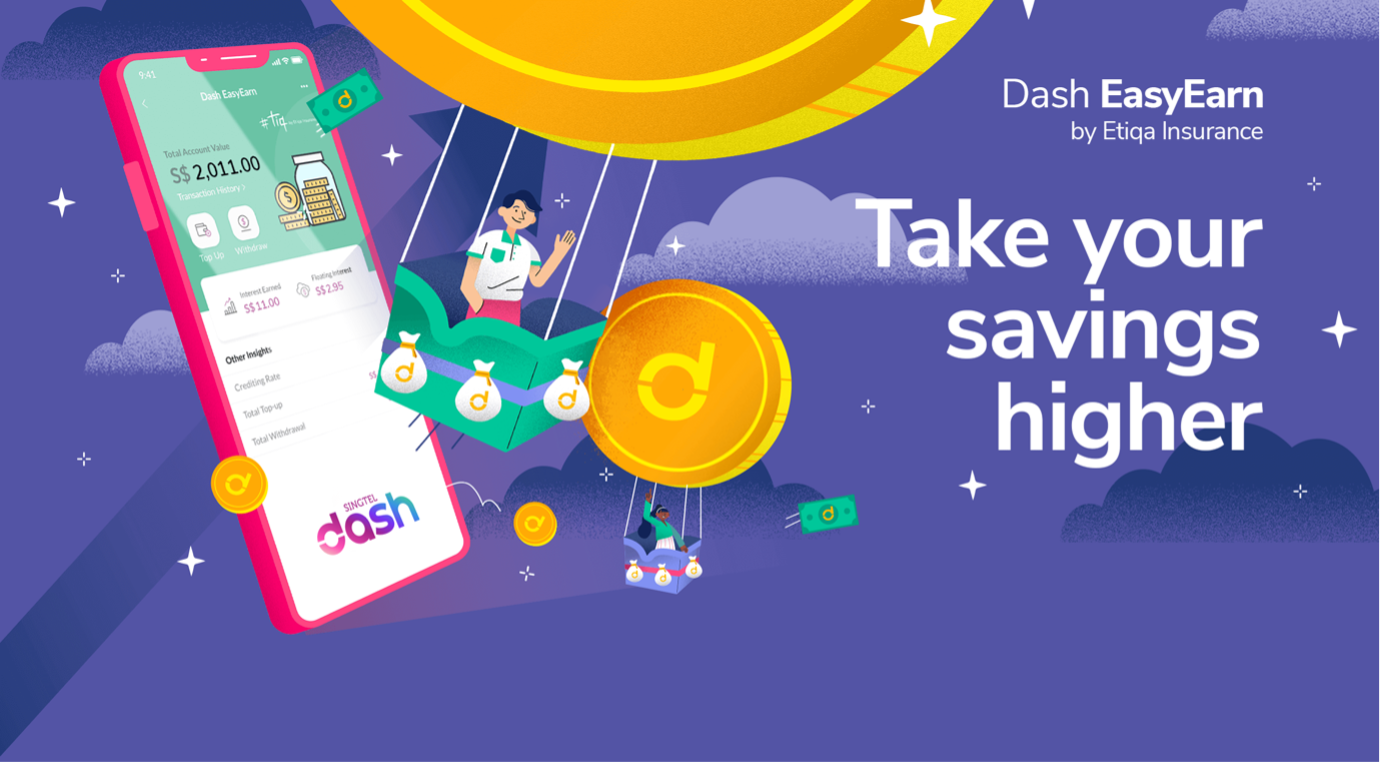

Singtel Dash is a digital wallet, but it also offers an interesting savings plan in its Dash EasyEarn product offering. It is meant to offer a simple way for you to grow your savings and be insured at the same time. With Dash EasyEarn, you can earn a guaranteed 1.8% p.a. on your capital. And it doesn’t come with any lock-in period or requirements, which means you can withdraw it anytime.

Besides the relatively higher interest rate than banks, the other benefit of Singtel Dash is that you get to enjoy the other peripheral digital wallet services like digital payment, insurance and rewards.

Interest Rate: 1.8% p.a. for the first year

Additional Bonus: 0.25% p.a. when you purchase additional protection plans with eTiQa

Minimum Premium: $2,000

Maximum Account Value: $20,000

Top-Up Available?: Yes

Requirement: TiqConnect app

Who’s Eligible: Singapore citizen, PR or Work Pass holder who are between 18 and 75 years old

With the 3 insurance savings plans that we introduced, it seems hard to beat such attractive offers. But we have something up our sleeves that can beat those 3 hands down. And that’s traded endowment!

If you haven’t heard about traded endowment, check out this traded endowment FAQ.

Traded endowments are actually pre-loved endowment plans that the original policyholder had to give up halfway before it has matured. Because of that, those who invests in traded endowments are able to reap the benefits of the previous policyholder for the number of years that he has already invested in the endowment plan.

While you don’t have the flexibility of withdrawing from the traded endowment anytime, the good thing is that traded endowments come with shorter maturity periods. This means you don’t have to worry that your money gets stuck in the traded endowment plan for too long! Not just that, the interest rate is also twice to quadruple of what you will earn with the 3 contenders that we listed above.

Interest Rate: 3% to 7.2%

Minimum Premium: Depends on the traded endowment plan

Maximum Account Value: Depends on the traded endowment plan

Top-Up Available?: No

Requirement: None

Who’s Eligible: Anyone

Get Your Traded Endowment Today!

Does traded endowment sound attractive to you? Interested in getting your traded endowment today? Reach out to us at Moneyline to find out what kind of traded endowment plans are available to you.

If you prefer the traditional endowment plans, you can also check out our endowment plans comparison article right here.

Comments are closed.

2 Comments